{kind=link}

The U.S. Prosecutors charge the BitMex founders Arthur Hayes, Benjamin Delo, Samuel Reed along with the senior manager Gregory Dwyer with (a) violating the Bank Secrecy Act and (b) conspiring to violate the Bank Secrecy Act, by willfully failing to establish, implement, and maintain an anti-money laundering (“AML”) program at the crypto exchange or BitMEX. The charges each carry a maximum penalty of five years in prison. (see DOJ press release). In a parallel action, the U.S. CFTC filed a complaint against the founders and their entities.

A 5-million bail

The U.S. Samuel Reed was the only one arrested. Warrants have been issued for BitMEX CEO and co-founder Arthur Hayes, co-founder Ben Delo, and head of business development Gregory Dwyer. Reed has been released on a $5 million bail, according to newly released court documents. Reed had to put up $500,000 in cash. Both he and his wife had to surrender their passports. He can only travel in New York, Massachusetts, and Wisconsin, with parole office approval. Reed is also banned from any contact with Hayes, Delo, or Dwyer without lawyers present.

Bribing offshore is cheap

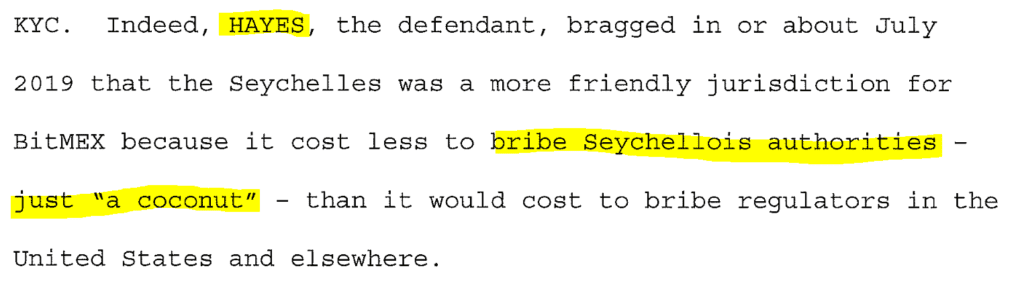

According to the indictment, the companies behind MitMEX were deliberately set up offshore because it would be easier to bribe the authorities and regulators there. Arthur Hayes is said to have bragged that it only costs “a coconut” to bribe the authorities in Seychelles.

According to the indictment, the companies behind MitMEX were deliberately set up offshore because it is easier to bribe the authorities and regulators there. Arther Hayes is said to have bragged that it only costs “a coconut” to bribe the authorities in Seychelles. Consequently, Hayes and his co-founders established HDR Global Trading Limited in Seychelles in 2014 to run the BitMEX crypto trading platform

One defendant went as far as to brag the company incorporated in a jurisdiction outside the U.S. because bribing regulators in that jurisdiction cost just ‘a coconut.’ The defendants will soon learn the price of their alleged crimes will not be paid with tropical fruit.

FBI Assistant Director William Sweeney

The CFTC, which filed a complaint against the founders and their entities, said in its press release that BitMEX’s platform “has received more than $11 billion in bitcoin deposits and made more than $1 billion in fees, while conducting significant aspects of its business from the U.S. and accepting orders and funds from U.S. customers.”

Offshoring in Cyprus

We do not want to claim that authorities in Cyprus take coconuts as a bribe. Heaven forbid! Formally, the EU member Cyprus is not even an offshore country either. In fact, Cyprus acts as an offshore country, selling citizenships to convicted criminals and being home to numerous big scam schemes and illegal payment processors. The Mediterranean island is well-known for its rather relaxed regulator, CySEC headed by Demetra Kalogerou.

The difference between the CFTC and CySEC could not be greater and one feels tempted to apply Arthur Hayes‘ statements about the “coconut states” in Seychelles to Cyprus as well. This difference in the respective approaches cannot be justified with “different legal situations” or “different regulatory regimes.” In the interest of injured investors and the security of the financial markets, the CFTC seeks disgorgement of ill-gotten gains, civil monetary penalties, restitution for the benefit of customers, permanent registration, and trading bans. While the CFTC – as regulators in the EU – started to chart the new crypto territory The Financial Ombudsman Office Cyprus, on the other hand, terminates well-documented and justified complaints.

People like the BitMEX founders are right with their analysis that in offshore countries it is much easier to circumvent laws and reassure authorities. Have they not?